![]()

5 Things We Learned This Week - 2/22/2025

Submitted by Silverlight Asset Management, LLC on February 22nd, 2025

Feb 22, 2025

The S&P 500 declined 1.6% this week. The Bloomberg Aggregate Bond Index gained 0.4%, gold rose 1.7%, and Bitcoin fell 2.6%.

Investors became skittish on Friday after a South China Morning Post report said a research team in China has identified a new bat coronavirus that could risk animal-to-human transmission. In other news, the Citi Economic Surprise Index fell to a five-month low this week after the S&P Global PMIs, University of Michigan Consumer Sentiment and Existing Home Sales reports weakened. Wal-Mart reported earnings this week and gave a cautious outlook on consumer spending. Investors will be closely watching the German snap election on Sunday for clues on the future policy direction for Europe's largest economy.

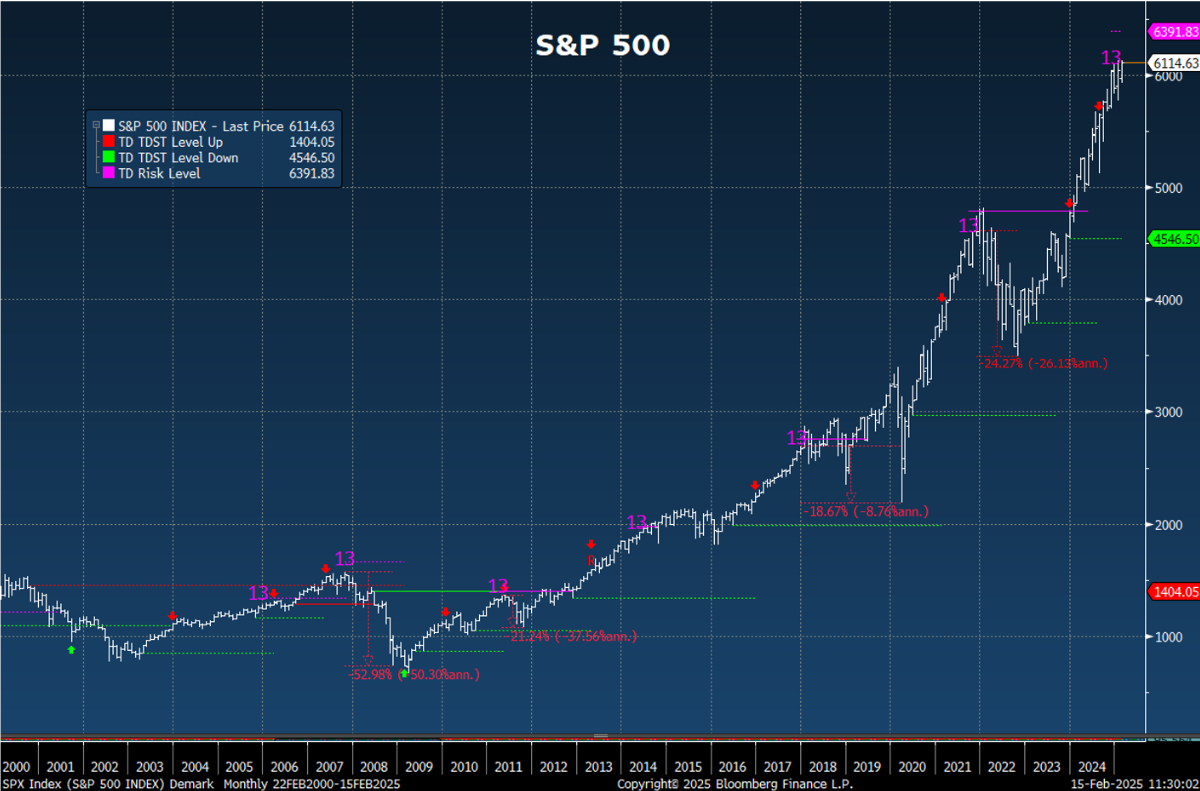

S&P 500 Prints Monthly DeMark Sell Signal

A trend is your friend, until it ends.

For many years, this blog has periodically highlighted DeMark indicators. DeMark is an objective market timing model that uses a price bar counting methodology and Fibonacci numbers to anticipate price levels where trend exhaustion is highly probable. While there are many nuances associated with this model, the most important takeaway for this post is that when a magenta 13 appears, trend reversals are likely.

In November 2024, a monthly 13 sell signal printed on the most important equity benchmark in the world—the S&P 500 index. This suggests a major market top is likely to occur in the next twelve months. The chart above was one of the most important slides in Michael Cannivet's Las Vegas MoneyShow presentation this week, titled: "How To Hedge The Next Bear Market." There have been seven TD Combo 13 sell signals on the monthly S&P 500 chart since 2000. The market experienced bear market declines of 20% or more in 5 out of these 7 cases. The worst drawdown was over 50% (2008), and the most recent sell signal appeared in late-2021, foreshadowing a 20% decline in 2022. If Silverlight clients are wondering why we have been raising extra cash in portfolios lately, now you know why. We protected capital in 2022 by raising cash early, and we will tread carefully this year until there is sufficient evidence to label this a false sell signal.

How Federal Layoffs Could Reshape the Housing Market

Efficiency today might mean a housing hangover tomorrow. Federal layoffs, often pitched as streamlining, could jolt the national housing market in unexpected ways. As government jobs vanish—especially in hubs like Washington DC—early signs point to trouble. Zillow reports 20% of DC’s 2,400 listings emerged in just two weeks, with 17% cutting prices, hinting at oversupply and weakening demand. Though federal workers are a small workforce slice, their economic footprint isn’t. Lost incomes shrink buyer pools, stalling sales nationwide. With mortgage rates hovering above 7% and existing home inventory at 4 million by late 2024—highest since pre-COVID—the market’s already on edge. Layoffs could tip it further as displaced workers sell. Beyond DC, expect echoes in states like California or Virginia with big federal presences. Consumer spending dips, confidence wanes, and suddenly, a seller’s market flips.

Since the pandemic, housing inventories have been artificially suppressed because so many homeowners have lower mortgage rates on their existing properties than they would receive if they refinanced a new property at prevailing market rates. In certain regions, the DOGE project will probably upend this paradigm and instigate price discovery that leads to a dip in prices. Thus far, national home prices remain sturdy. But we are also seeing early signs of rising inventory in previously hot areas like Florida and Texas, where a lot of new supply has recently been built.

Microsoft and Apple's Valuations Mirror Each Other

Over the last decade, Microsoft has beat Apple in innovation. Microsoft's strategic pivot to the cloud and its $13 billion investment in OpenAI have paid dividends, integrating AI into its suite of products and enhancing user experiences. Conversely, Apple's focus has largely been on iterative iPhone updates, with its most ambitious projects—like the Apple Car and the high-priced Vision Pro headset—not yielding any significant breakthroughs.

Since that is the case, can anyone explain why Microsoft and Apple's price-to-sales ratios (PSR) have both expanded by 11% per year over the last decade? Ten years ago, Microsoft and Apple traded at a PSR of about 4. Today they are both near a double-digit multiple. This doesn't make a lot of fundamental sense. Ten times sales is super expensive, especially if we're talking about the biggest companies in the world, where the law of large numbers naturally restricts future growth potential.

Valuation is also an expression of relative sentiment. Why is the market just as giddy about Apple as Microsoft, even though the last major innovation at Apple happened on Steve Jobs' watch well over a decade ago?

In our view, this odd valuation dynamic is further evidence of a broader passive investing bubble. For the last decade, Microsoft and Apple have occupied around the same weights in the S&P 500. As more and more money has dripped into index funds like SPY, the companies at the top are probably getting an automatic bid, which results in an artificial valuation bump. If we are right and flow dynamics are indeed driving stock valuations more than fundamentals, it probably means the biggest stocks will do best in bull markets and be extra vulnerable in bear markets.

The GLP-1 Shortage Ends: Implications for NVO, LLY & HIMS

The FDA recently declared the Ozempic and Wegovy shortage resolved as of February 21, 2025, after Novo Nordisk ramped up production to meet soaring demand. This is a win for Novo Nordisk, and led to a 13% rally this week. It enhances competition with Eli Lilly, whose Zepbound shortage ended in December. The two companies dominate the global weight loss drug market, which is projected to exceed $150 billion by 2030. Silverlight managed portfolios own both NVO and LLY.

The restored supply chain is bad news for Hims & Hers (HIMS), a telehealth provider of compounded semaglutide. Silverlight was long HIMS, but we sold last week after our price objective was met. This turned out to be a lucky and well-timed exit. After the GLP-1 news broke on Friday, HIMS fell 25%.

We All Stand on the Shoulders of Giants

In Las Vegas this week, the author of this blog got to meet one of his heroes, Tom DeMark. Tom invented the model that appears in this week's first story back in the 1970s, and he has served as a key advisor to multiple stars from the hedge fund world, including Steve Cohen and Paul Tudor Jones. Tom also presented at the MoneyShow this week, in what might be his final conference appearance. Not only did he proactively come over to the Silverlight booth to introduce himself, but he also invited us to dinner! Turns out, one of the greatest market timers of his generation also happens to be a really nice guy from Racine, Wisconsin.

Another interesting encounter from the conference involved a 17-year old attendee. The young man's mother brought him to the conference because he's fascinated by investing. He quizzed me for tips on how to build an investment process, similar to how I spent the previous evening picking Tom's brain. Driving home from the event, I realized the only reason I'm in a position to advise a young person about anything in this field is because of my mentors who paved the way. Whatever we do, whoever we are, we all stand on the shoulders of giants.

Multi-generational mentoring is awesome. It pays to seek out mentors and to be one. When you mentor someone, being mentored at the same time keeps you humble and curious. It’s a reminder that no one has all the answers, no matter their experience level. A mentor might teach resilience, while a mentee shares insights on adaptability in a fast-changing world. This reciprocal process fosters empathy, breaks down generational silos, and builds more inclusive communities.

This material is not intended to be relied upon as a forecast, research or investment advice. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by Silverlight Asset Management LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Silverlight Asset Management LLC, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Testimonials Content Block

More Than an Investment Manager—A Trusted Guide to Financial Growth

"I’ve had the great pleasure of having Michael as my investment manager for the past several years. In fact, he is way more than that. He is a trusted guide who coaches his clients to look first at life’s bigger picture and then align their financial decisions to support where they want to go. Michael and his firm take a unique and personal coaching approach that has really resonated for me and helped me to reflect upon my core values and aspirations throughout my investment journey.

Michael’s focus on guiding the "why" behind my financial decisions has been invaluable to me in helping to create a meaningful strategy that has supported both my short-term goals and my long-term dreams. He listens deeply, responds thoughtfully, and engages in a way that has made my investment decisions intentional and personally empowering. With Michael, it’s not just about numbers—it’s about crafting a story of financial growth that has truly supports the life I want to live."

-Karen W.

Beyond financial guidance!

"As a long-term client of Silverlight, I’ve experienced not only market-beating returns but also invaluable coaching and support. Their guidance goes beyond finances—helping me grow, make smarter decisions, and build a life I truly love. Silverlight isn’t just about wealth management; they’re invested in helping me secure my success & future legacy!"

-Chris B.

All You Need Know to Win

“You likely can’t run a four-minute mile but Michael’s new book parses all you need know to win the workaday retirement race. Readable, authoritative, and thorough, you’ll want to spend a lot more than four minutes with it.”

-Ken Fisher

Founder, Executive Chairman and Co-CIO, Fisher Investments

New York Times Bestselling Author and Global Columnist.

Packed with Investment Wisdom

“The sooner you embark on The Four-Minute Retirement Plan, the sooner you’ll start heading in the right direction. This fun, practical, and thoughtful book is packed with investment wisdom; investors of all ages should read it now.”

-Joel Greenblatt

Managing Principal, Gotham Asset Management;

New York Times bestselling author, The Little Book That Beats the Market

Great Full Cycle Investing

“In order to preserve and protect your pile of hard-earned capital, you need to be coached by pros like Michael. He has both the experience and performance in The Game to prove it. This is a great Full Cycle Investing #process book!”

-Keith McCullough

Chief Executive Officer, Hedgeye Risk Management

Author, Diary of a Hedge Fund Manager

Clear Guidance...Essential Reading

“The Four-Minute Retirement Plan masterfully distills the wisdom and experience Michael acquired through years of highly successful wealth management into a concise and actionable plan that can be implemented by everyone. With its clear guidance, hands-on approach, and empowering message, this book is essential reading for anyone who wants to take control of their finances and secure a prosperous future.”

-Vincent Deluard

Director of Global Macro Strategy, StoneX